JNU research team re-publishes paper in top journal

JNU research team re-publishes paper in top journal

Date: 3rd June, 2020

Source: College of Information Science and Technology

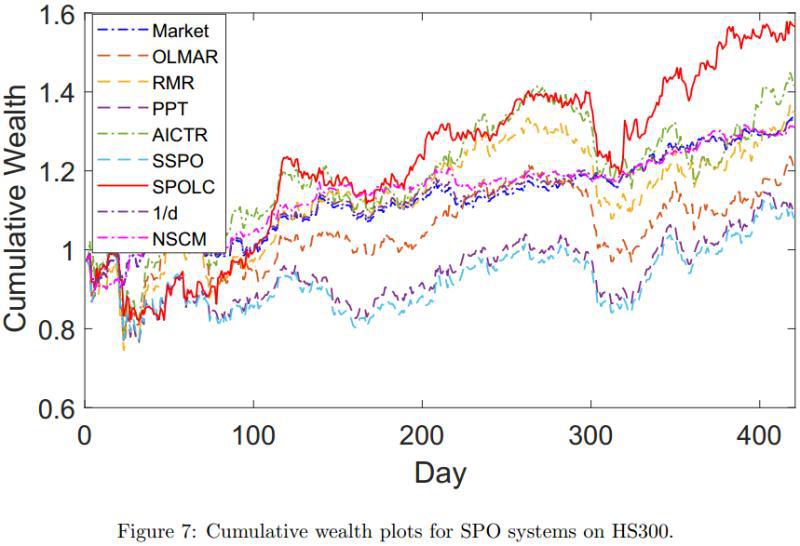

The paper Loss Control with Rank-one Covariance Estimate for Short-term Portfolio Optimization by Lai Zhaorong and his team from JNU's College of Information Science and Technology, the Guangdong Provincial Engineering Research Center for Quantitative Finance and Big Data, and the Laboratory of Intelligence and Data Security, has been published by Journal of Machine Learning Research (JMLR), a top-level international journal in the computer field. All of the paper's authors come from JNU. Lai, an associate professor in the mathematics department, is the first author and corresponding author. The co-authors are Tan Liming, a 2018 postgraduate in the College of Economics and previously an undergraduate in the mathematics department, and Wu Xiaotian and Fang Liangda, both associate professors in the computer science department.

In this paper, Lai's team reconsiders the role of covariance estimation from the perspective of operators and their spaces. They also appropriate an estimation of covariance in all primary rank-one covariance spaces containing observation matrices and establishing a mechanism to control investment losses to better capture instantaneous risk structures.

The research is supported by the Guangdong Provincial Engineering Research Center for Quantitative Finance and Big Data and the Laboratory of Intelligence and Data Security. It is financed by JNU's Talent Introduction Research Start-Up Fund, the National Natural Science Foundation Youth Project, the National Natural Science Foundation, the National Special Fund for Basic Scientific Research in Colleges and the operating expenses of the Guangdong Provincial Engineering Research Center for Quantitative Finance and Big Data.

NEWS

- About the University

- Quick Links

Copyright © 2016 Jinan University. All Rights Reserved.